Vacation, all I ever wanted. Vacation, got to get away. Preferably no less than two times a year and ideally for a week at a time to properly forget all about my worries and responsibilities and everything else that comes with day-to-day life. While I love daydreaming about spending a week in the Greek isles, I don’t always love the harsh reality that is the price tag associated with travel. Often, my Instagram inspired goals exceed my budget, and life becomes a game of balancing. We’ve learned a lot about budgeting and planning vacations in the 10+ years we’ve been together, so below, I share what we’ve found to be the best ways to save money for vacation so you can swim with the dolphins or enjoy the fireworks over Cinderella’s castle after a day at Disney.

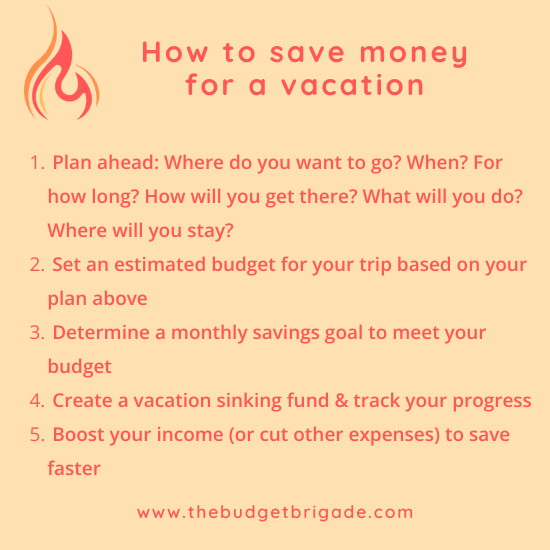

Plan ahead for your next vacation

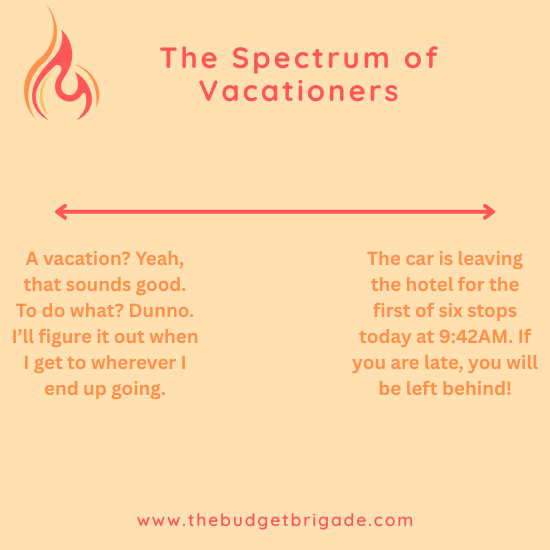

Some people enjoy the whimsical nature of taking their explorations one day at a time and seeing which ways the winds take them. Others are maniacal planners who need every minute of a trip planned down to the last detail.

While thankfully neither my husband nor I are on the far ends of the vacationer spectrum, we tend toward opposite sides. As a former logistics coordinator, I like to have an itinerary planned out before we leave for a trip. My husband prefers to pick a place and then figure out what to do once we get there.

To say you should plan ahead for a vacation doesn’t mean you have to know every single detail. But it’s important to know the basics, especially if you’re worried about how you’re going to pay for the trip. Consider:

- Where do you want to go?

- When do you want to go?

- For how long?

- Where will you stay? A hotel? Airbnb? With family or friends?

- How are you going to get there? Plane? Train? Automobile?

- What types of activities do you hope to do?

If you’ve always swiped and put vacations on a credit card and then had to pay interest because you couldn’t pay it all off, it’s going to take a mind shift to save for your next trip. Planning is a superpower here. It gives you time to save so you don’t have to go into debt and suffer from a vacation spending hangover the next month. And the next. And the month after that.

The decision for each question above will impact what your vacation costs and thus what you’ll need to save in order to afford it. Hiking, for example, can be free, while taking a dog sled across the frozen tundra or a helicopter sightseeing excursion will set you back a pretty penny. Flying overseas will cost way more than driving two hours to your destination.

Set an estimated budget for your trip

By planning ahead, you can estimate what the trip will cost to give you an idea of what your savings goal needs to be. It’s important to note that tourism is often seasonal and businesses charge accordingly. This is why we recommend setting a timeframe for when you want to go during your planning stage. If you’re planning to fly to Colorado during peak skiing season, be prepared to pay more for hotels and flights. Spring break in Florida? Good luck scoring a decent hotel for anywhere near reasonable.

If you want to go to New Zealand in three months but you haven’t saved anything, it likely isn’t going to happen. But New Zealand in two years? That’s probably doable, especially if you’ve already built up an emergency fund and tackled all your high-interest debt using the debt snowball or debt avalanche method.

If you haven’t done these yet, pause here and seriously consider taking a break from vacations for a short season to get yourself into a better financial position where you’ll actually be able to enjoy your trips versus still coming home just as stressed to a big money mess. Or take that time off so you don’t lose it, but do something cheaper that you can easily cash flow while hammering out your financial goals.

When estimating your budget, I always like to pad it so that you risk of having too much saved versus running out of money during your trip. You can always splurge on a fancy dinner at the end of the trip with the excess, but the sushi place won’t take refunds from the week before so you can afford the gas to drive the last leg home. And if you don’t use your entire vacation budget, you can roll it into the next one! What a perfect excuse to go somewhere else or do something new and exciting one weekend near home.

Pro tip: you can plan and save for more than one vacation at a time! We had a goal to take a once-in-a-lifetime trip to Norway to see the Northern Lights. We wanted to go all out and do an upscale cruise. When we saw the price tag, we gulped. It was going to take a while. We saved and planned for over a year and a half. But we didn’t waste our PTO during that time. We budgeted and saved for a few road trips to some really cool places while we saved up for the big trip. We planned each trip separately with different budgets and savings goals.

Use your planning to set a monthly savings goal

Now you’ve got a plan for what you want to do, an idea of when you hope to go, and an estimate of how much it will cost. With these three magic pieces to the vacation puzzle, you can set a monthly savings goal. Take how much you need to save and divide it by how long you have to save.

Example: Valentine’s Day for John and Jane

John and Jane hope to spend Valentine’s Day in Las Vegas next year. They plan for a four day long weekend. Using Google Flights, they see that flights are much cheaper if they leave Wednesday and fly back Saturday, and they’re okay flying back on the evening of actual Valentine’s Day to save a pretty penny because they’re ballers on a budget. Flights from Salt Lake City where they live are $426 round trip total for the pair of them if they do basic economy. While they’d love to fly first class, it’s only an hour and a half flight, so they’ll survive.

They’d love to stay somewhere like the Bellagio, but plugging their dates into Hotels.com suggests they can expect to pay around $1,300 for their planned stay. Yikes. The New York-New York hotel just down the Strip comes out to around $450 instead, or about a third of the cost. For that much savings, they can walk a bit to see the fountain show.

They’ve never been to the Grand Canyon, so they want to use one of the days to road trip and see it. Jane doesn’t know it yet, but John’s planning on proposing. To get to the Grand Canyon, they’re going to need to rent a car. Orbitz helps them estimate the cost of a rental car. Being out on the open road where cell service is spotty and gas stations, let alone towns, are 100+ miles apart, they opt to splurge here and skip the rental car companies that have a 30% positive rating and instead settle on Thrifty or Dollar, which at least top a 50% approval. They estimate their rental car will cost $243. Gas prices that far out are hard to predict, so they aim high at $4 a gallon, which helps pad mileage driving around Las Vegas too and for stops. Google maps clocks their trip at 561 miles, so Jane rounds it up to 600 and targets 25 mpg. Quick math tells her they should budget around $96 for gas, so they make it $100. They have a national parks pass, so they won’t have to pay to explore the Grand Canyon. John’s already saving up for the ring, so he doesn’t need to plan for that as part of the vacation expenses.

Jane’s a bit of a foodie, and they want to make sure they get to take in at least one nice buffet. While in Vegas, baby! They budget $75 a person per day for meals, drinks, and snacks and then plan to use whatever is remaining to buy souvenirs before they head home. $75 for each of them for four days is (gulp) $600. They might back that down when they actually get to Vegas but hey, better to plan for the worst and have leftover.

John’s sister lives close to them in Salt Lake City and is willing to drop them off and pick them up at the airport, so thankfully they won’t have to pay for parking there. They will, however, have to pay for parking at the hotel in Las Vegas, which is another $20 a day.

Along with exploring the Strip and going to the Grand Canyon, they want to see Penn & Teller live and, of course, spend some time in the casinos. Tickets to the show claim to be $64.50 but by the time the site adds all the stupid fees, they’re looking at closer to $165 total. Neither of them gamble much, so they decide on $100 each for the slots.

So now they have their estimate cost for the Valentine’s Day John hopes is their best yet (God, if she says no when he pops the question, he might just jump into the Grand Canyon):

- Airport parking: $0

- Airfare: $500 (they round up to be safe and to adjust for prices in the future)

- Rental car + gas: $350

- Hotel & hotel parking: $530

- Food & souvenirs: $600

- Entertainment: $365

Total Vegas trip: $2,345.

To make Mr. Monk happy, they decide to set a savings goal of $2,500. John and Jane are both saving steadily for retirement already, and John will have his credit card debt paid off well before the trip, even if he slows down his extra payments in order to save, so they decide this is a reasonable plan.

With eight months to save, they need to save $312.50/month. Knowing that they’ll have to prepay certain expenses such as the airfare and Penn & Teller tickets, they make a mental note to book those in the coming months once they have enough.

This is John and Jane’s fake situation, though I used the sites above to pull actual numbers at the time of writing this article to help provide a real world(ish) example.

Before we jump into how to save the money for the trip, I want to caveat our advice so far to say if you aren’t saving for retirement but you’re shoveling away a lot of money for vacation, consider revisiting your budget and reassessing priorities. You want to be saving some for the future before spending the rest in the present. Vacations, after all, are also great to have in retirement when you have a shitload of free time on your hands. Don’t rob from your future to YOLO in the present, but also make sure you’re enjoying your time today instead of leaving all your travels until you’re old when your hip might not be up for it.

Explore our basics of investing guide.

Create a vacation sinking fund and track your progress

With your savings goal (in Jane and John’s case, $312.50/month, or $156.25 each a month) in hand, it’s important to keep track of your progress and to set that money aside, marked especially for your vacation.

Sinking funds are my favorite way to save money, especially for vacation. Having that money in a special fund earmarked just for the trip allows me to enjoy myself guilt free once the vacation finally arrives. My husband enjoys this too because even if the hotel ends up not being what he expected, he’s less disappointed because he’s already spent the money in his mind. It’s gone already, so there’s less pressure to make the most of it. If, however, he was trying to figure out how he was going to pay for the hotel at the end of the month, he’d go full blow Karen and be super stressed.

We like to leave our vacation sinking fund in a high-yield savings account. We keep it in the same account as our emergency fund, but I have a simple spreadsheet I update at the end of each month when we’re doing the budget for the next month that tells me what money I have allocated to each fund.

Updating my sinking funds with the budget at the end of the month helps me track our progress, which keeps me motivated. It can also let you know when you can go book flights or pay for show tickets, if you’re John and Jane.

Boost your income (or cut other expenses) to fund your vacation budget

If your kid is dying to go on a Disney cruise for their 10th birthday and you are dying to get out of the cold and escape to the Caribbean for a week, you might want to pack up and go, even if your wallet says no.

We want you to find a way, but we don’t want you to go into debt to do so. If your vacation planning doesn’t line up with what you can realistically make happen, consider adding some temporary income to save up enough.

Weighing the opportunity cost of your time against the cost of the vacation can also help you decide how badly you want to go versus finding something cheaper as an alternative. Explore side hustle ideas in our entrepreneurship station.

If you have the money but it seems to disappear to other places throughout the month, like Chick-fil-A or Starbucks, consider setting up your monthly savings goal as an automatic transfer from your checking account to your high-yield savings account. Just think of it like a bill you’ve got on autopay. Future Jane is billing today’s Jane for February’s fun.

Also take the time to look at where specifically that money evaporates to. Okay, fine, it was Chick-fil-A. God, when did chicken get so expensive?!?! See if you can cut back on your dining out budget for the next few months. Or maybe you have a bunch of subscriptions you should probably cancel, especially since you forgot you even had them and were paying for them. Anywhere you can find to trim back your budget is extra money you don’t have to go out and earn.

Explore 13 ways to cut spending and save money on a tight budget.

Need help staying inspired?

I’m all about vision boards. If you’re struggling to save up for your vacation, bookmark some of your favorite photos from your destination that you’ve found online. Pull up the hotel website once in a while and remind yourself of all the amenities that await (oh, a sauna!).

And always feel free to drop a line in our budgeting and personal finance Facebook group, where we’d be happy to cheer you on to help you stay on track.

Enjoy your trip!

The best part about intentionally savings money for vacation is actually twofold:

One: There is power and pleasure in delayed gratification. Our culture is becoming more and more centered on instant dopamine hits from instant gratification. That’s why we open our Facebook app six times in an hour to see if anyone has liked or commented on our post since we last checked. (Come on, I know that’s not just me, right?)

It’s awesome to always have a vacation planned on the horizon. We booked our Norway vacation over a year before the actual trip, and I got to be excited about that vacation for months on end. Whenever someone was spamming my feed with gorgeous pictures of the aurora, I got a dopamine hit about our trip to chase the Northern Lights. And when it felt like I was standing on the surface of the sun in the summer, I just pictured myself looking like Kristoff in Frozen.

Since I didn’t actually get to see the Northern Lights, you might even say the anticipation was a better payoff than the delivery of the trip for that specific part. (Though sadly, it turns out it really is that cold in Norway in February; no wonder Olaf wanted to do whatever it was that snow does innnnnn summerrrrrrr.)

Two: When you’ve budgeted and saved for a vacation, there is zero guilt in spending that money within your budget when vacation time comes around. As someone who admittedly struggles with a scarcity mindset around money, it’s hard for me to enjoy spending money on fun things. Having a big, healthy vacation sinking fund helps. Because we’ve budgeted that money specifically for fun, and the money we’ve saved for vacations is a reasonable part of our income, it isn’t a pinch we’re trying to make happen. Instead, it’s something I can enjoy guilt free, and without the stress of how in the world I’m going to pay for it all, which makes the trip that much more enjoyable.

Explore more ways to travel on a budget

- Intentional spending versus FOMO for vacations

- How to road trip on a budget

- How to eat cheap on vacation

Have a travel question you’re dying to ask? Ask us your budgeting question today.